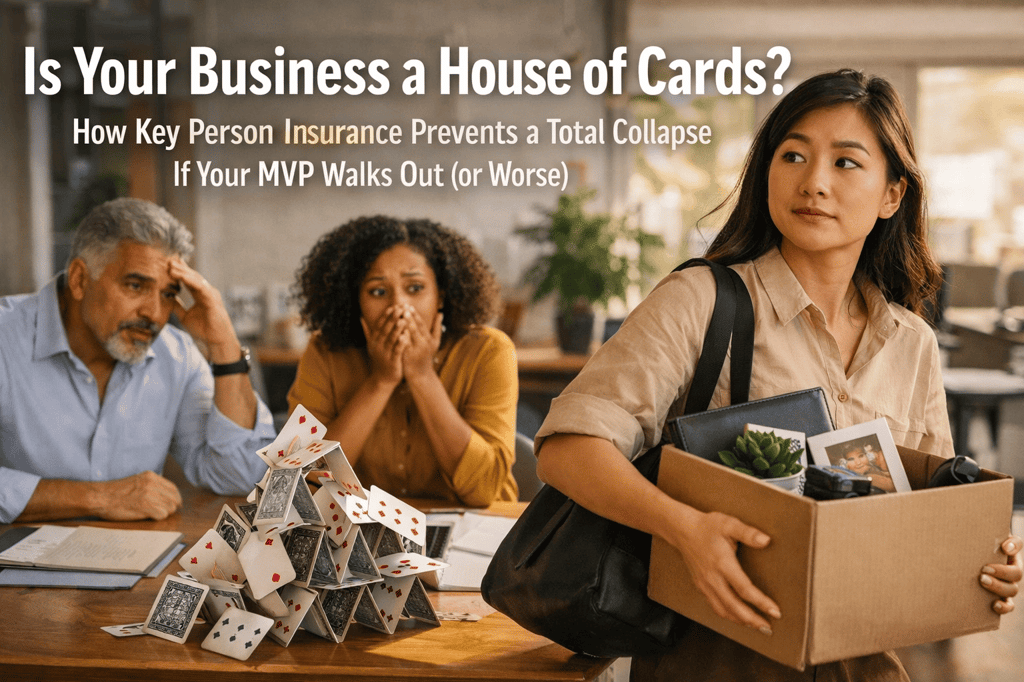

Is Your Business a House of Cards? How Key Person Insurance Prevents a Total Collapse If Your MVP Walks Out (or Worse)

Don't let your business collapse if a key employee leaves. Learn how Key Person Insurance provides the financial shock absorber your company needs to survive.

BUSINESS OWNER STRATEGIES

Uju M.

2/22/20266 min read

You built your business from the ground up. You know every client relationship. You've perfected the systems. You are the systems.

And that's exactly the problem.

Most business owners don't realize they're sitting on a ticking time bomb. Your company's success isn't just tied to your products or services: it's tied to specific people whose departure could trigger a complete operational collapse. We're not talking about theoretical risk here. We're talking about the brutal reality that if your top salesperson, lead engineer, or visionary founder disappears tomorrow, your business could be facing a financial catastrophe within weeks.

Key Person Insurance exists for exactly this moment: the moment when your business's most valuable asset walks out the door, and you need immediate cash to survive the transition.

The House of Cards Effect: When One Person Holds Everything Together

Here's what most business owners won't admit out loud: their entire operation depends on one or two critical people.

The sales director who personally handles 60% of revenue. The technical founder whose expertise is irreplaceable. The operations manager who keeps every system running smoothly. These aren't just employees: they're load-bearing pillars holding up your entire structure.

When one of these pillars suddenly collapses, the domino effect is immediate and devastating. Client relationships evaporate. Projects stall. Revenue plummets. Team morale tanks. And you're left scrambling to find a replacement while watching your cash flow hemorrhage in real time.

The timeline is brutal. It can take six to twelve months to recruit, hire, and train someone capable of filling those shoes. During that period, your business still has payroll to meet, overhead to cover, and debts to service: all while operating at a fraction of normal capacity.

This isn't pessimism. This is risk management financial planning at its most essential.

What Key Person Insurance Actually Does (And Why It's Not Optional)

Key Person Insurance is a life insurance policy your business purchases on the individuals whose loss would create immediate financial hardship. You own the policy. You pay the premiums. And if that key person dies or becomes critically disabled, your business receives a death benefit that functions as a financial shock absorber during the crisis.

Think of it as emergency capital that appears exactly when your business needs it most: when everything else is falling apart.

The death benefit isn't pocket money. It's designed to cover the real costs of sudden loss: recruiting expenses for replacement talent, training costs, lost revenue during the transition, ongoing overhead, and debt obligations that don't pause just because your world stopped.

For small businesses and startups without deep financial reserves, this isn't a luxury: it's the difference between surviving and shutting down.

The Financial Lifeline Your Business Doesn't Know It Needs

Here's what happens when a key person dies without insurance protection in place:

Your business immediately faces a cash flow crisis. Revenue drops because that person's relationships, expertise, or reputation drove significant income. Meanwhile, your fixed costs remain unchanged. Payroll still needs to be met. Rent is still due. Loan payments don't pause for tragedy.

Without an immediate capital infusion, you're forced to make impossible choices. Do you lay off other employees to stay afloat? Do you take out high-interest emergency loans? Do you sell equity at a desperate valuation just to keep the lights on?

Key Person Insurance eliminates these impossible choices by providing instant liquidity. The death benefit gives you breathing room to execute a thoughtful transition plan instead of making panic decisions that damage your business long-term.

Coverage That Matches Your Actual Risk

The typical coverage amount ranges from 5 to 10 times the key person's annual salary: but that's just a starting baseline. The real calculation should be based on their actual monetary contribution to your business.

If your lead salesperson generates $2 million in annual revenue, losing them doesn't just cost you their $150,000 salary: it costs you the revenue pipeline they managed, the client relationships they maintained, and the institutional knowledge they carried.

You have options for policy structure:

Term policies provide coverage for specific periods: typically 10, 20, or 30 years. These are more affordable and work well if you expect the business to become less dependent on specific individuals over time as systems mature and teams deepen.

Permanent policies offer lifetime coverage with a cash value component that builds over time. These cost more upfront but create an asset your business can leverage later while maintaining protection indefinitely.

The choice depends on your business stage, growth trajectory, and cash flow planning priorities. Early-stage companies often start with term coverage and upgrade to permanent policies as revenue stabilizes.

Protection Strategies for Different Business Structures

Your business structure changes how Key Person Insurance functions: and how critical it becomes.

Partnerships and multi-owner businesses face unique vulnerability. When one partner dies, surviving partners need capital to buy out the deceased partner's share from their heirs. Without funding in place, you're forced to negotiate with grieving family members who may want immediate payout or involvement in business decisions they don't understand. Key Person Insurance provides the buyout capital needed to maintain control and execute succession plans smoothly.

Sole proprietorships have different concerns. If you die, your heirs inherit not just your business assets but also your business debts. Key Person Insurance ensures they have funds to settle obligations and either continue operations or close the business in an orderly fashion: not a fire sale that destroys value.

Loan requirements often mandate Key Person Insurance as collateral. Financial institutions and investors understand business concentration risk better than most owners do. They require insurance to protect their capital if you lose a critical team member. This isn't banks being difficult: it's lenders forcing you to address a risk you should be managing anyway.

The Ownership Structure That Protects Everyone

Your business owns the policy, pays the premiums, and receives the death benefit. The insured employee must provide written consent, but they don't own or control the policy: you do.

This structure keeps things clean. The insurance isn't a personal asset for the employee. It's a business asset designed to protect business continuity. When structured correctly, the death benefit generally comes to your business tax-free, providing maximum financial impact exactly when you need it most.

The premiums themselves aren't typically tax-deductible as business expenses, but that's a small price compared to the protection you're receiving. You're essentially pre-funding your own crisis response plan: building a financial safety net that activates automatically when disaster strikes.

Why This Matters More Than You Think

Business owners consistently overestimate their company's resilience and underestimate their dependence on key individuals. It's human nature. You've built systems and processes. You have a team. Surely the business could survive without any single person.

But the market doesn't care about your optimism. Clients don't care about your succession plans. When the person they trust disappears, they start evaluating alternatives immediately. Your competitors smell blood in the water and start circling. Your team loses confidence. The entire ecosystem that supports your business begins questioning whether you can survive.

Key Person Insurance sends a different message. It tells clients, employees, lenders, and partners that you've thought about worst-case scenarios and funded solutions in advance. It demonstrates the kind of risk management financial planning that separates businesses built to last from businesses hoping nothing goes wrong.

More importantly, it gives you options when you have none. It provides capital when traditional funding disappears. It creates stability when everything around you is chaos.

Building a Business That Survives You

The hardest truth in business ownership is this: your company's success shouldn't depend on your immortality.

Every business eventually faces transition: whether planned or unexpected. The businesses that survive these transitions are the ones that prepared for them. They identified their key person dependencies. They quantified the risk. And they funded protection strategies that turn potential catastrophes into manageable transitions.

Key Person Insurance is how you build that protection. It's how you ensure that your business: and everyone who depends on it: doesn't collapse when the unthinkable happens.

This isn't about pessimism or fear. It's about building something bigger than yourself. It's about creating a business that can survive the loss of any single person, including you: because you planned ahead and funded the solutions your business would need in crisis.

At Dynasty Founders, we help business owners identify concentration risks and structure protection strategies that preserve what they've built. Because your business deserves to outlive its founders.

The question isn't whether you need Key Person Insurance. The question is whether you're willing to bet your business that nothing will ever happen to the people holding it all together.

Most houses of cards eventually fall. The ones that don't are built on stronger foundations: foundations that include financial strategies designed for worst-case scenarios.

Build the foundation. Protect the people. Secure the future.

Your business: and everyone counting on it: deserves nothing less.

Ready to identify your business's key person risks and build protection strategies that work? Schedule a free consultation with Dynasty Founders and discover how to turn vulnerabilities into strengths.

We do not respond to unsolicited domain, SEO, or marketing solicitations.

© 2025. All rights reserved.

Services

Income Protection

Tax-Free Retirement

Wealth Accumulation

IUL Insurance

Estate Planning

Company

Get started

Empowering families and communities with the financial knowledge and tools to build lasting wealth and secure their legacy.